Read this article in 中文 Français Deutsch Italiano Português Español

LNG market expected to remain tight through 2025

March 06, 2023

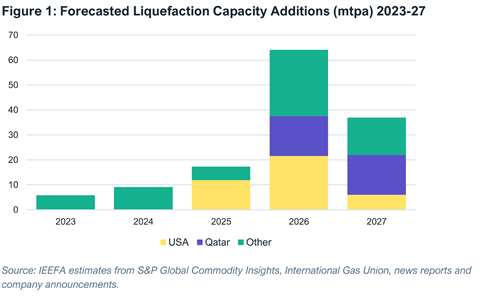

The study from IEEFA shows a surge in export capacity starting around mid 2025.

The study from IEEFA shows a surge in export capacity starting around mid 2025.

Global LNG supplies are likely to remain tight over the next two years in the face of strong demand in Asia and Europe, but that demand should fade by 2030 as decarbonization and energy security policies take effect, a recent study shows.

Meanwhile, a wave of new LNG export capacity coming online later in the decade could create a mismatch between supply and demand, elevating financial risks for LNG suppliers and traders.

The findings come from the new Global LNG Outlook from the Institute for Energy Economics and Financial Analysis (IEEFA), which analyzes LNG supply and demand developments in Europe, Asia, Australia, the U.S., and Qatar. The report concluded that last year’s LNG market turmoil, marked by record high prices and unreliable supplies, has undermined long-term demand in both Europe and Asia.

The study noted that in 2022, European countries boosted LNG imports by 60% to make up for declining pipeline gas shipments from Russia. Europe’s red-hot LNG demand drove global spot prices to all-time highs, forcing price-sensitive Asian buyers to slash LNG purchases and curtail plans for new LNG imports.

China cut 2022 LNG purchases by 20%, due to a combination of high prices, COVID-19 shutdowns, and slower economic growth. High LNG prices have pushed the country’s gas buyers to rely more heavily on domestic production and pipeline imports.

India, Bangladesh, and Pakistan slashed LNG demand by a combined 16% last year. Concerns over fuel security, unaffordability, rapidly depleting foreign currency reserves, and demand destruction could limit the region’s medium-term LNG imports, the study concluded.

Southeast Asian countries face both high prices and infrastructure constraints. In addition, long-term LNG contracts with deliveries starting before 2026 are reportedly sold out globally, forcing Southeast Asian countries to turn to the spot markets to fill local needs, which can be more expensive.

In Japan and South Korea, high LNG prices led to a resurgence of nuclear power generation that could slash long-term demand for gas in the power sector. In Taiwan, persistent terminal delays and state-owned utility financial difficulties could constrain rapid increases in LNG imports.

Europe’s demand for LNG should remain strong in 2023, but could fall after that as EU climate and energy security policies curtail gas demand by at least 40% through 2030.

Although new LNG terminals could boost the continent’s import capacity by one-third by the end of 2024, Europe’s ambitious energy transition targets mean that much of the new capacity could remain unused, according to the study.

The Russia-Ukraine crisis has exposed long-term financial risks throughout the LNG value chain. In 2022, high spot prices and supply disruptions earned LNG a reputation as an expensive and unreliable fuel source, undermining the prospects for demand growth in key markets. When large volumes of new supply enter the market starting in mid-2025, it could trigger a supply glut, heightening the financial and pricing risks for LNG exporters and traders.

MAGAZINE

NEWSLETTER

CONNECT WITH THE TEAM