Gas Production, Exports Likely To Rise: EIA

February 19, 2020

While gas prices hit a 20-year low this month and gas reserves have already reached record levels in the U.S., the U.S. Energy Information Administration is still projecting that gas production won’t be really slow down much in the foreseeable future.

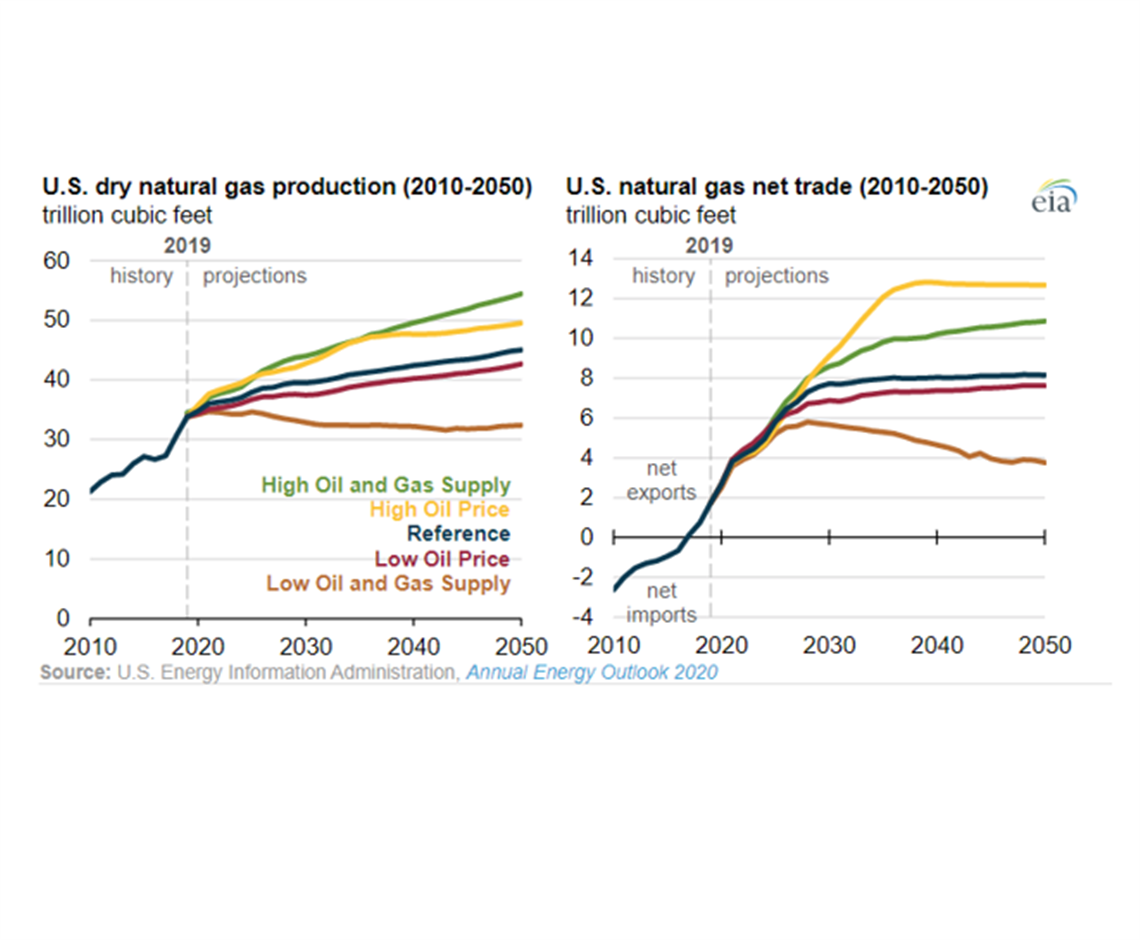

According to projections published in EIA’s Annual Energy Outlook 2020 (AEO2020), total dry natural gas production in the United States will continue to increase until 2050 in most of the AEO2020 cases, primarily to support growing U.S. exports of natural gas to global markets. The United States began exporting more natural gas than it imports on an annual basis in 2017, driven by increased liquefied natural gas (LNG) exports, increased pipeline exports to Mexico, and reduced imports from Canada. In most of the AEO2020 cases, net natural gas exports continue to increase through 2050, and most of the increase is in the near term.

The AEO2020 Reference case represents EIA’s best assessment of how U.S. and world energy markets will operate through 2050, assuming no significant changes in energy policy occur. Side cases show the effects of changing model assumptions: the High and Low Oil Price cases simulate international conditions that could drive crude oil prices higher or lower, and the High and Low Oil and Gas Supply cases vary production costs and resource recoverability within the United States.

The AEO2020 Reference case represents EIA’s best assessment of how U.S. and world energy markets will operate through 2050, assuming no significant changes in energy policy occur. Side cases show the effects of changing model assumptions: the High and Low Oil Price cases simulate international conditions that could drive crude oil prices higher or lower, and the High and Low Oil and Gas Supply cases vary production costs and resource recoverability within the United States.

EIA expects dry natural gas production to total 34 tcf in 2019 once the final data is in. In the AEO2020 Reference case, EIA projects that U.S. dry natural gas production will reach 45 tcf by 2050. Production growth results largely from continued development of tight and shale resources in the East, Gulf Coast, and Southwest regions, which more than offsets production declines in other regions. Dry natural gas production from these three regions accounted for 68% of total U.S. dry natural gas production in 2019 and, in the Reference case, 78% of dry natural gas production in 2050.

Most of the increase in dry natural gas production is coming from natural gas formations such as the Marcellus and Utica in the East region and the Haynesville in the Gulf Coast region. A smaller but still significant portion of the growth is from associated gas production in oil formations, especially in the Permian Basin in the Southwest region.

In the Reference case, both U.S. natural gas exports by pipeline and U.S. LNG exports continue to grow through 2030. LNG exports account for most of the export growth because more LNG export facilities are becoming operational and more projects are under construction. In the Reference case, EIA projects that LNG exports will almost triple, from 1.7 tcf in 2019 to 5.8 tcf in 2030, the equivalent of nearly 16 bcfd. LNG exports remain at this level through 2050 as U.S.-sourced LNG becomes less competitive in world markets and as more countries become global LNG suppliers.

In the Reference case, both U.S. natural gas exports by pipeline and U.S. LNG exports continue to grow through 2030. LNG exports account for most of the export growth because more LNG export facilities are becoming operational and more projects are under construction. In the Reference case, EIA projects that LNG exports will almost triple, from 1.7 tcf in 2019 to 5.8 tcf in 2030, the equivalent of nearly 16 bcfd. LNG exports remain at this level through 2050 as U.S.-sourced LNG becomes less competitive in world markets and as more countries become global LNG suppliers.

U.S. LNG exports are more competitive when oil prices are high (as in the High Oil Price case) and U.S. natural gas prices are low (as in the High Oil and Gas Supply case) because of pricing structures that link Brent crude oil prices to LNG prices in many world markets. In the High Oil Price case, U.S. natural gas net exports reach nearly 13 tcf by the late 2030s, most of which is LNG. Conversely, in the Low Oil Price case and Low Oil and Gas Supply case, U.S. LNG is less competitive globally and remains lower than 5 tcf per year through 2050.

By comparison, pipeline trade of U.S. natural gas is less sensitive to changes in assumptions about domestic natural gas supply and world oil prices. Pipeline trade of natural gas is highest in the High Oil and Gas Supply case because low domestic natural gas prices reduce U.S. natural gas imports from Canada.

By comparison, pipeline trade of U.S. natural gas is less sensitive to changes in assumptions about domestic natural gas supply and world oil prices. Pipeline trade of natural gas is highest in the High Oil and Gas Supply case because low domestic natural gas prices reduce U.S. natural gas imports from Canada.

MAGAZINE

NEWSLETTER

CONNECT WITH THE TEAM