Regional Report: China’s changing gas dynamics

28 September 2022

A liquified natural gas (LNG) tanker leaves the dock after discharge at PetroChina’s receiving terminal in Dalian, Liaoning province, China in July 2018. (Photo: Reuters.)

A liquified natural gas (LNG) tanker leaves the dock after discharge at PetroChina’s receiving terminal in Dalian, Liaoning province, China in July 2018. (Photo: Reuters.)

Downward pressure on China’s natural gas demand has resulted in the country’s LNG imports dropping off, even as it continues to expand its regasification capacity.

Chinese natural gas dynamics are changing as the country receives more imports from Russia while its LNG purchases decline as a result of depressed demand. This represents something of a retreat after China overtook Japan to become the world’s largest LNG importer in 2021 but could now drop back to second place.

Nonetheless, the buildout of Chinese regasification capacity is set to continue, but potentially with less urgency in the near term as downward pressure persists on domestic gas demand. Over the longer term, though, the country will likely still expect its gas demand to grow.

Recent developments

Recent changes have helped shape the way China’s gas infrastructure and broader gas market have been developing. Particularly significant among these is the creation of PipeChina to take over midstream infrastructure from the country’s national oil companies (NOCs) and encourage the participation of new players in the sector.

“The China Oil & Gas Pipeline Network Corporation (PipeChina) was formed in December 2019 to provide neutral access to the country’s pipeline infrastructure to all qualified users including non-state-owned companies,” GlobalData’s practice head of energy research, Sumit Kumar Chaudhuri, told COMPRESSORtech2. “The pipeline reform along with bullish forecasts for LNG demand encouraged several smaller domestic players to get involved in LNG procurement.”

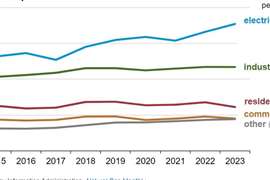

According to GlobalData, Chinese LNG imports rose from 60.1mn tonnes in 2019 to 68.0mn tonnes in 2020 and 72.7mn tonnes in 2021.

“China witnessed a significant increase in LNG import volumes and to support this surge several LNG receiving terminals (both new and expansions) have been announced in recent years,” said Chaudhuri.

However, new downward pressures on demand have since emerged, especially over the past year.

Demand down

Factors weighing on Chinese gas demand currently include Beijing’s Zero-Covid policy, which has looked increasingly futile in the face of the more transmissible Omicron variant of Covid-19. China has persisted with it, though, responding to new outbreaks of the virus with lockdowns that have hit economic growth and energy demand.

Meanwhile, gas and LNG prices have risen, especially in the wake of Russia’s invasion of Ukraine in February. With the war in Ukraine continuing and Europe scrambling to reduce its dependence on imports of Russian energy while global supplies remain tight, gas prices are expected to remain high for the time being. Given China’s depressed demand, this has deterred the country from buying LNG on the spot market.

“China’s gas demand has been under pressure since Q4 2021 due to the economic slowdown, higher import prices and a rebound in coal consumption,” a Wood Mackenzie vice president and head of Asia-Pacific, gas and LNG research, Valery Chow, told COMPRESSORtech2. “More recently, Covid outbreaks and widespread lockdowns have dealt a major blow to energy demand, including natural gas,” Chow continued. “LNG imports have been hit the hardest, dropping by 21% year-to-date so far. Buyers have minimized their exposure to costly spot LNG.”

As a result, some regasification terminals are currently operating below their full capacity. “There have been noticeably fewer takers for PipeChina’s spare LNG terminal slots,” Chow said.

This has translated into more LNG available to Europe that would have otherwise gone to China, notably LNG produced in the US. Indeed, declining demand has had an impact on contracted volumes as well as those available on the spot market.

“China’s national oil companies have been diverting contracted cargoes to Europe, profiting from the significant arbitrage,” Chow said.

Closer partnership

At the same time, though, China has been snapping up Russian natural gas and LNG at discounted prices as Western countries have shunned Russian energy. According to Wood Mackenzie, Chinese LNG imports from Russia hit a two-year high in August. And Russian gas is not flowing to China in the form of LNG alone.

“During the first half of 2022, China recorded high pipeline gas imports from Russia via the Power of Siberia pipeline,” Chaudhuri said. “In addition to this, China recently struck a deal with Russia’s Sakhalin-2 LNG plant to purchase LNG at half the current spot prices. With this new deal and the undergoing construction of Phase 2 of the Power of Siberia pipeline, the flow of Russian gas to China is expected to increase gradually.”

Wood Mackenzie also anticipates closer energy ties between China and Russia in the future.

“China will be Russia’s primary target customer for both pipeline and LNG sales going forward,” Chow said. “Russia will be looking to fast-track development of Power of Siberia 2 pipeline, which would divert previously Europe-bound gas from Western Siberian fields to China via Mongolia.”

This shift in gas flows is expected to be beneficial to both Russia and China over the longer term.

“China will welcome the opportunity to secure more and cheaper gas supplies in the coming years as part of its longer-term ambition to phase down coal consumption,” Chow said. “With Europe effectively cut off, Russia will be anxious to pivot east to anchor long-term gas sales. Closer China-Russia energy co-operation is of mutual benefit and builds on the strengthening relationship between both countries.”

There are still plenty of unknowns, including questions over how the war in Ukraine will ultimately come to an end. However, even after it ends, European demand for Russian gas currently looks unlikely to return, especially if consumers in Europe are successful in replacing Russian imports with other sources of supply such as additional LNG from the US.

In the shorter term, there are further uncertainties relating to winter demand and Beijing’s Covid-19 policy that could have an impact on gas price movements.

“The major risk factors lie in a cold winter and/or a potential relaxation of Covid rules after the 20th National Congress of the Chinese Communist Party in October,” said Chow. “As Chinese buyers go head-to-head in competition with Japanese, Korean and European buyers, this would exacerbate an already tight and volatile global price environment.”

Regasification outlook

For now, Wood Mackenzie anticipates that Chinese demand for LNG will remain depressed at least for the remainder of the year.

“Downward pressure is expected to persist for the remainder of 2022,” said Chow. “Over 2022 gas demand is anticipated to grow by 2% year on year, but year-on-year LNG imports are forecast to drop by 12% to 70mn tonnes. This unprecedented decline means that China will cede the title of world’s largest LNG importer back to Japan.”

Despite this, China’s regasification capacity build-out is set to continue, with the country expecting to rely on gas more heavily in the future.

GlobalData estimates that China has announced 5.72 Tcf (1.62 × 1011 m3) of newbuild regasification capacity and 1.33 Tcf (3.77 × 1010 m3) of capacity from expansions that are due to be added by 2026. However, GlobalData estimates only 3.35 Tcf (9.49 × 1010 m3) of newbuild capacity and 582.48 Bcf (1.65 × 1010 m3) of expansion capacity additions are already at the advanced stage of development and under construction.

“We understand that this capacity is more firm or, has greater likelihood of getting added by 2026,” Chaudhuri said.

Wood Mackenzie also expects that China’s regasification capacity will expand significantly over the remainder of the decade, despite the current demand dynamics.

“The bulk of China’s extensive regasification capacity buildout was already in operation or under construction prior to 2022,” said Chow. “We anticipate a doubling of total capacity by 2030 from current levels of around 105 mtpa. Projects in proposal stages are targeting first gas beyond 2026, which is when we expect LNG prices to soften materially with the additional of significant new LNG supply from Qatar and the US.”

Certain projects now under development represent particularly significant additions to Chinese regasification capacity. In a release put out earlier this year, GlobalData noted that Tangshan II was the largest upcoming regasification project in China, with a capacity of 584.4 Bcf (1.66 × 1010 m3) by 2026. The consultancy added that the Yantai I and Zhoushan III projects, with capacities of 487.0 Bcf (1.38 × 1010 m3) and 340.9 Bcf (9.65 × 109 m3) respectively, were other major projects.

Aside from these, Chaudhuri identified two further projects that are worth watching as they represent particularly sizeable capacity additions. The first of these is Binhai.

“This regasification project of CNOOC at Yancheng (Jiangsu Province), with a regasification capacity of 292.2 Bcf [8.27 × 109 m3], would be associated with 10 large LNG storage tanks with total storage capacity of 1.2 million tonnes,” Chaudhuri said. “The terminal is expected to be operational by December 2023. Further expansion proposed for this terminal includes increasing its capacity to 438.3 Bcf [1.24 × 1010 m3] and adding 10 more LNG storage tanks post-2026.”

The other project identified by Chaudhuri as being worth watching is Qingdao Phase III.

“Sinopec is working on the third expansion phase of the Qingdao LNG terminal to increase its capacity from 340.9 Bcf [9.65 × 109 m3] to 681.8 Bcf [1.93 × 1010 m3] by the end of 2023, making it the largest LNG terminal in China in 2026.”

GlobalData declined to estimate Chinese gas pipeline capacity over the coming years, given the lack of validated up-to-date information on such capacity. However, the country’s pipeline capacity is likely to grow alongside its regasification capacity.

LNG sale and purchase agreements (SPAs) struck by Chinese companies with producers of the fuel – notably in the US – in recent months also indicate that China expects its gas demand to grow over the longer term. These SPAs have been agreed both by smaller companies and NOCs. PetroChina struck a deal to buy LNG from the US’ Cheniere Energy in July, while both CNOOC and Sinopec signed SPAs with Venture Global LNG in late 2021. Chinese buyers have also recently started signing SPAs to buy LNG from US export projects that have yet to reach the final investment decision (FID) stage, helping to take those projects a step closer to going ahead.

Negotiating SPAs is a lengthy and complex process, so those deals announced in recent months are likely to have been under discussion for a considerable amount of time prior to being finalised. However, the upheaval in global gas markets in the wake of Russia’s invasion of Ukraine may well have added a sense of urgency to negotiations.

Separately, media reported in June that Chinese NOCs were in advanced talks over a potential investment in Qatar’s North Field East expansion, which is the world’s single largest liquefaction project. Nothing further has been reported, and the NOCs have not commented publicly on the matter.

It is unknown whether the current pressures on demand will cause China to rethink its approach to LNG. However, the country will be keen to shield itself from further volatility in the spot market, and it is likely that over the longer term, it still expects to require more natural gas, including to help it cut back on coal use.

If Chinese gas demand unexpectedly drops again in the future, there will be more possibilities of diverting contracted LNG cargoes to other countries like it has been doing this year. However, it seems unlikely that current dynamics have dented the country’s longer-term expectations.

MAGAZINE

NEWSLETTER